IAIS - International Associations of Insurance Supervisors

December 2023

Reinsurance Report Highlights

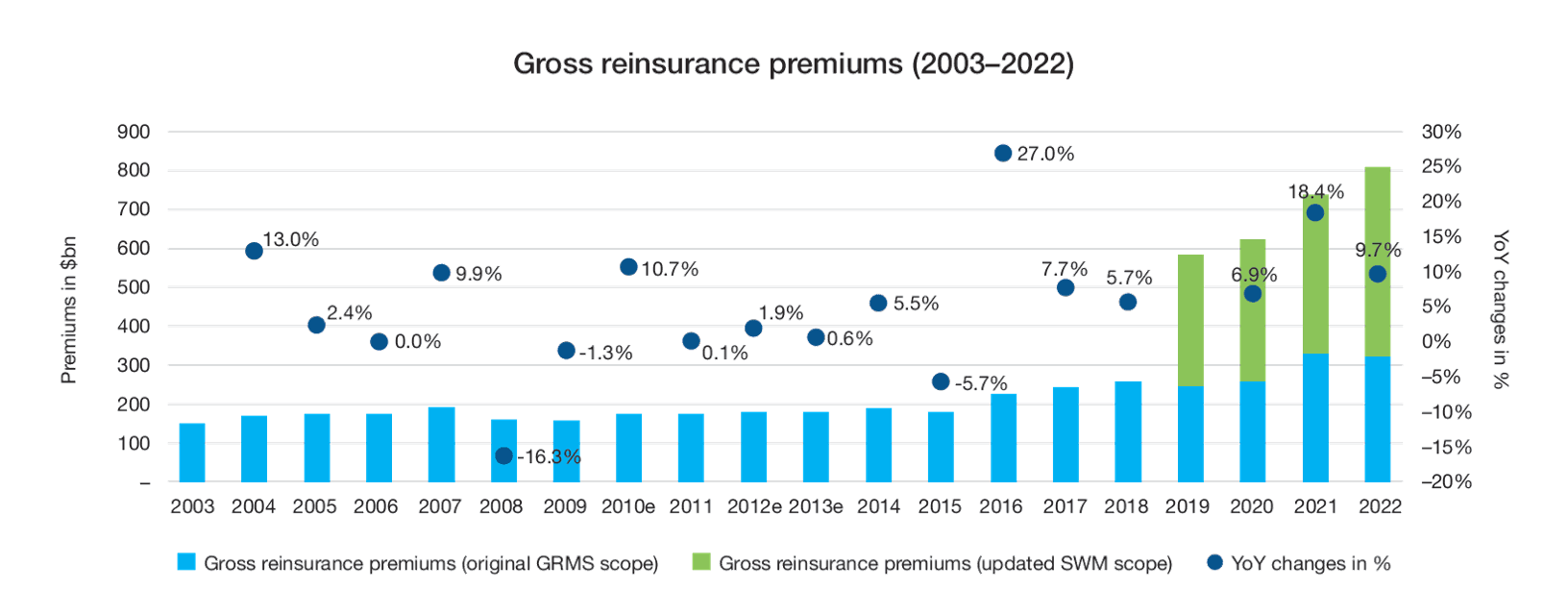

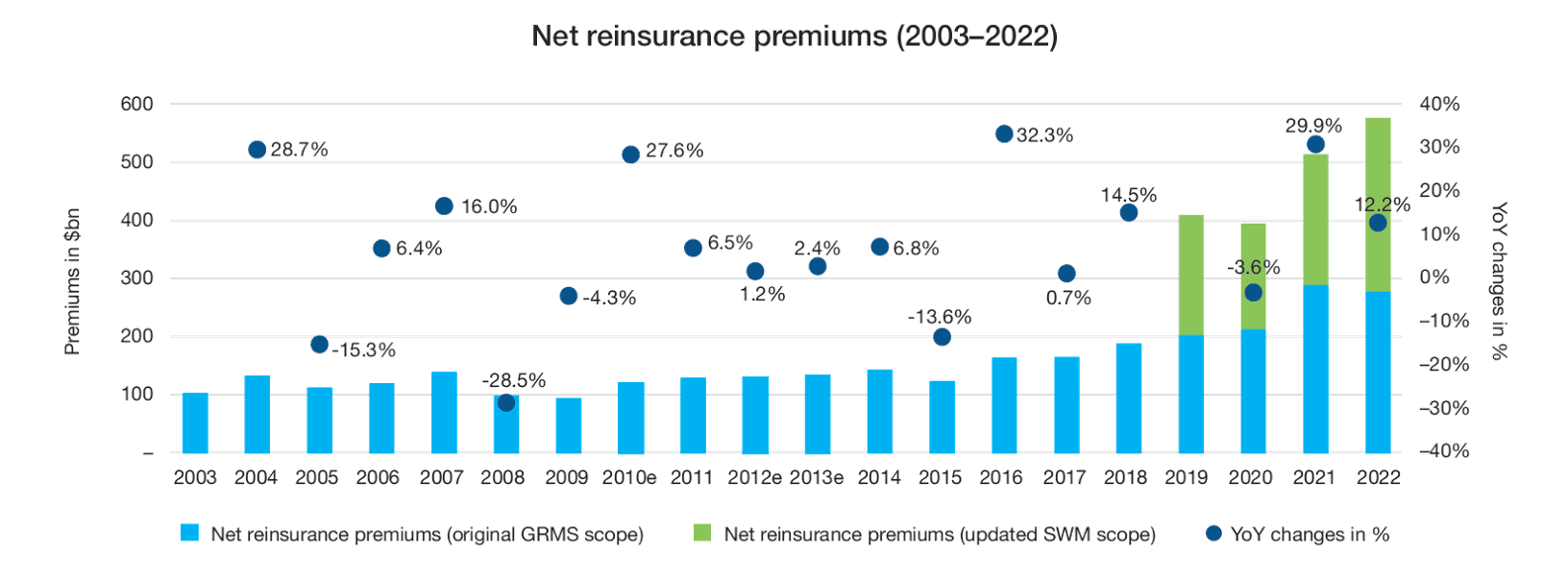

From 2003 to 2019, the IAIS collected data on the global reinsurance market through its annual Global Reinsurance Market Survey (GRMS). The GRMS covered about 50 reinsurers based in nine jurisdictions: Bermuda, France, Germany, Japan, Luxembourg, Spain, Switzerland, the UK and the US. The GRMS collected data from reinsurers with gross unaffiliated reinsurance premiums of more than $800 million or unaffiliated gross technical provisions of more than $2 billion. The pool of participating reinsurers remained largely the same throughout this period.